Application blueprint

Step-by-step recipe for an event study from data ingestion to publication-ready test statistics.

New to event studies?

This page is the practical how-to: it walks through the decisions and steps required to run an event study, from identifying the event date to choosing windows, models, and significance tests. If you first need the concepts (what an event study is, how the efficient-market rationale justifies it, and how abnormal returns and their aggregates are defined), start with the introduction to the methodology, which explains what an event study is and how abnormal returns are calculated. The blueprint below assumes those definitions and links back to them at each step.

The step-by-step procedure

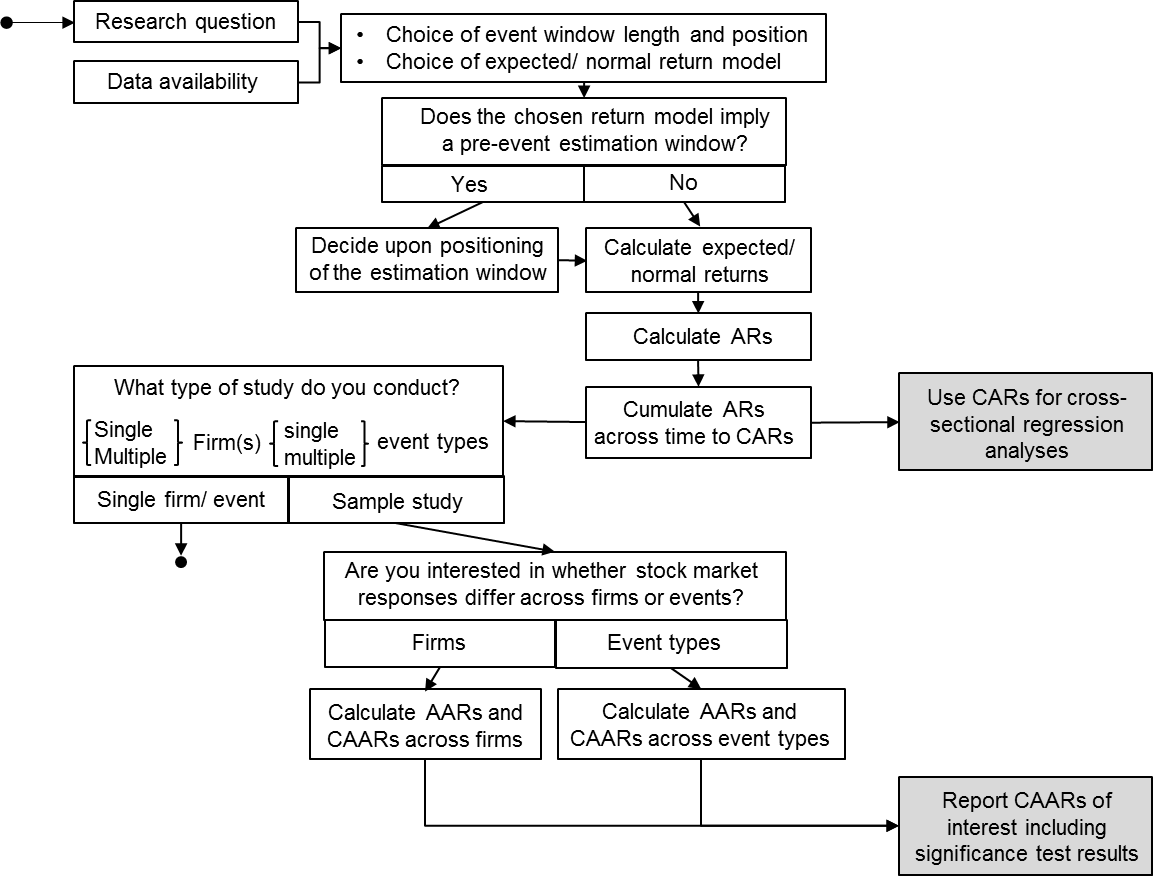

Event studies follow a uniform workflow ("blueprint") that consists of methodological choices and analytical steps. While researchers may use a dedicated tool for the analysis, they should be knowledgeable about the overall workflow and its implied choices. The numbered procedure below follows the canonical sequence set out in the methodological literature (MacKinlay, 1997; Kothari & Warner, 2007). Figure 1 illustrates the same workflow as a flowchart.

- Identify the event and the event date. Define the event of interest and fix the event date (t=0) that anchors the analysis. On what date did the market first receive the information? See Identifying the event date below.

- Select the sample and screen for confounding events. Assemble the firms (and their event dates) to be studied, then remove or flag observations whose estimation or event windows are contaminated by other material news. See Confounding events below.

- Choose an expected/normal return model that matches your research question and data availability. Pick the model first because it determines whether you need an estimation window at all. See Choosing a model and a significance test and the full survey on expected return models.

- Set the lengths and positions of the estimation and event windows. Decide how long the estimation window is, how far it sits before the event, and how wide the event window is around t=0. See Choosing the lengths of the estimation and event windows below.

- Estimate normal returns and compute abnormal returns. Estimate the model parameters over the estimation window (for the market model, alpha and beta by OLS), then compute the abnormal return as observed return minus normal return for each firm and day in the event window. Aggregate across time into cumulative abnormal returns (CARs), across firms into average abnormal returns (AARs), and across both into cumulative average abnormal returns (CAARs). For the formulas and the two-axis intuition, see AAR, CAR and CAAR in the introduction; for the parameter estimation, see the market model.

- Run significance tests. Establish whether the abnormal returns found at the AR, AAR, CAR, or CAAR level are statistically significant. See significance tests and the selection guidance below.

Figure 1: Event Study Blueprint

Own Illustration

Identifying the event date

The event date is the anchor of the whole analysis, and fixing it correctly is not always a simple task. In the analysis of M&A transactions, for example, initial rumors about the transaction are typically followed by an official announcement and later a closing. On each of these dates information is released, posing the question of which date represents the correct event date. Scholars investigating this issue found the information content of the first official announcement to be highest, making it the correct event date in the context of M&A studies (Dodd, 1980). Similar questions arise when studying other event types: the rule of thumb is to anchor on the date the market first received credible, material information. Where many event dates must be located across a large sample, you can identify event dates with EDI.

Choosing the lengths of the estimation and event windows

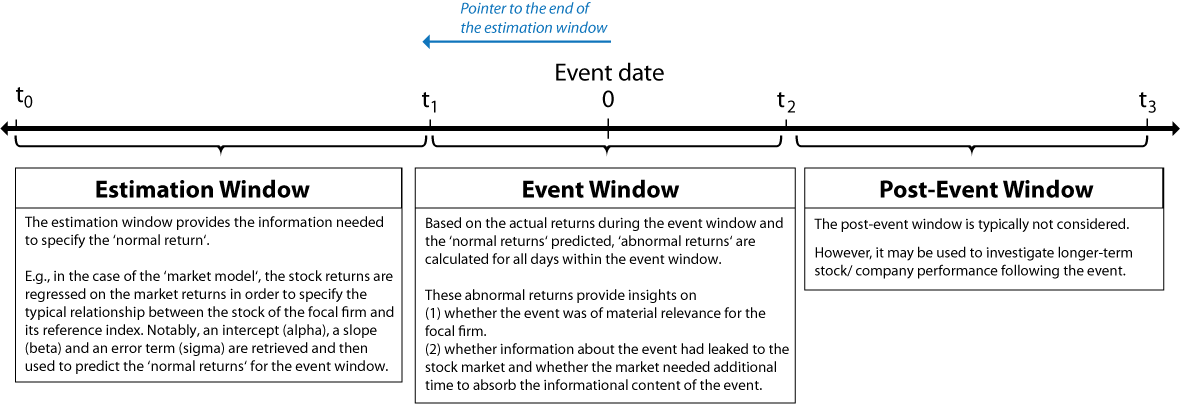

Depending on the choice of expected/normal return model, event studies either imply the use of an event window only (e.g., the market-adjusted model) or both an event and an estimation window (e.g., the market model). Most commonly the market model is used. It predicts normal returns with a regression that regresses stock returns on market returns over the estimation window, capturing the typical relationship between the stock and its reference index in two parameters (alpha, beta); the regression itself is explained in the market model. Figure 2 sketches the data structure used by event studies and shows how the market model uses it.

Figure 2: Data Structure of Event Studies with an Estimation Window

Adapted from Benninga (2008: 372)

There is no definite rule on the length of an event study's estimation and event windows: researchers have a discretionary choice. With regard to the estimation window, the challenge is to balance a tradeoff between improved estimation accuracy and potential parameter shifts. Longer estimation windows promise greater accuracy, because they imply larger samples of returns, but they also raise the risk of covering structural breaks (e.g., due to confounding events) in the alpha and beta parameters, which biases the estimators. A similar challenge applies to the event window: one must specify the period over which the event impacted the stock. On the one hand, information leakage and longer information-processing periods favor longer event windows; on the other hand, the risk of confounding events favors shorter ones.

The empirical evidence frames these choices. Recent meta-research reviewing 400 event studies finds that estimation-window lengths spread between 30 and 750 days (Holler, 2014). Studies investigating the sensitivity of results (e.g., the predicted return on the event date) suggest that results are not sensitive to varying estimation-window lengths as long as the window exceeds about 100 days (Armitage, 1995; Park, 2004). As a recognizable canonical reference point, MacKinlay's (1997) worked example uses a 250-day estimation window alongside a 41-day event window for daily data. Event windows themselves typically range between 1 and 11 days and center symmetrically around the event day (Holler, 2014). A roughly 5-day window was the single most common choice, used in 76.3% of the studies surveyed (Oler, Harrison & Allen, 2008). Taken together, a short symmetric event window of about 5 days centered on t=0, paired with an estimation window of at least 100 days (commonly 120 to 250 trading days) that precedes and does not overlap the event window, is a defensible default.

Confounding events

A confounding event is any other material news (earnings releases, dividend changes, litigation, unrelated corporate actions) that affects a firm's stock during the windows you are studying. Confounding events matter in two places. First, in the estimation window they can cause structural breaks in alpha and beta and bias the normal-return estimates, so screen the estimation window for contamination and exclude or re-time affected observations. Second, in the event window they make it impossible to attribute the abnormal return to your event alone, which is the main reason to keep the event window short: the wider the window, the higher the chance of catching unrelated news. Document your screening criteria so the isolation of the event is defensible.

Data choices

Several practical data decisions shape the results at the margin. Daily returns give finer event-window resolution and are standard for short-horizon studies, while monthly returns are sometimes used for long-horizon designs. Returns can be computed as simple returns or as log (continuously compounded) returns; be consistent throughout. For the reference index, choose between a value-weighted and an equal-weighted market index (or a broad benchmark such as the S&P 500): value-weighted indices track large-cap behavior, equal-weighted indices give small firms more influence. Match the index and return interval to your sample and state the choices explicitly. The conceptual background to these choices is covered briefly in the introduction.

Choosing a model and a significance test

Which expected-return model. Use the market-adjusted model when an estimation window is impractical (it needs none); use the market model as the workhorse when you have a clean estimation window; reach for factor models (Fama-French 3/5 or Carhart) when size, value, or momentum exposures could confound the result, especially in long-horizon designs. This is a selection decision only: for the full comparison of models and their usage shares, see expected return models.

Which significance test. The parametric t-test is the baseline, but use a standardized cross-sectional test (Patell, or the Boehmer-Musumeci-Poulsen test) when the event itself induces extra return variance; use nonparametric sign or rank (Corrado) tests when returns are non-normal or samples are small. Again this is a selection decision: the test battery and worked examples live on significance tests.

Tools: run it with ARC

You do not have to implement this workflow by hand. The Abnormal Returns Calculator runs every step above, from normal-return estimation to test statistics: run it with the ARC calculator. ARC ships with sensible defaults that mirror the guidance on this page, including a 250-day estimation window, so you can reproduce the canonical setup and then adjust the windows and model to your design.

References

The sources cited above are listed below; for the full bibliography see references.

- Armitage, S. 1995. Event study methods and evidence on their performance. Journal of Economic Surveys, 9(1): 25-52.

- Benninga, S. 2008. Financial modeling (3rd ed.). Cambridge, MA: MIT Press.

- Dodd, P. 1980. Merger proposals, management discretion and stockholder wealth. Journal of Financial Economics, 8(2): 105-137.

- Holler, J. 2014. Event-Study-Methodik und statistische Signifikanz. Oldenburg.

- MacKinlay, A. C. 1997. Event studies in economics and finance. Journal of Economic Literature, 35(1): 13-39.

- Oler, D. K., Harrison, J. S., & Allen, M. R. 2008. The danger of misinterpreting short-window event study findings in strategic management research: an empirical illustration using horizontal acquisitions. Strategic Organization, 6(2): 151-184. (2007 SSRN working paper; published 2008.)

- Park, N. K. 2004. A guide to using event study methods in multi-country settings. Strategic Management Journal, 25(7): 655-668.